The Strait of Hormuz Disaster: Why OXY Could Hit $120 by Fall

The Strait of Hormuz is not just another geopolitical flashpoint. It is one of the most important pieces of energy infrastructure on Earth, except it is not a pipeline, refinery, port, or oilfield. It is a narrow waterway connecting the Persian Gulf to the open ocean, and when it stops functioning normally, the global oil market stops behaving normally.

That is why Occidental Petroleum, better known by its ticker symbol OXY, has suddenly become one of the most interesting high-upside oil stocks in the market.

This is not because OXY is the biggest oil company. It is not. ExxonMobil and Chevron are larger, more diversified, and generally safer. But that is exactly the point. OXY is not the boring mega-cap way to bet on oil. It is a more leveraged, more volatile, more oil-sensitive vehicle. If the Strait of Hormuz remains effectively closed or severely restricted for months, OXY could become one of the cleaner ways to express a violent oil-price thesis.

The stock is currently around $58.71, giving it a market cap of roughly $57.8 billion. If the market begins pricing a prolonged Hormuz shutdown instead of a temporary disruption, a move toward $80 could happen quickly. A move toward $100 becomes plausible. And in a true sustained-crisis scenario, $120 by fall is no longer crazy. It is aggressive, but it is not fantasy.

The Strait of Hormuz Is the Oil Market’s Pressure Point

The reason this situation matters so much is simple: a massive amount of global oil has to pass through one narrow channel.

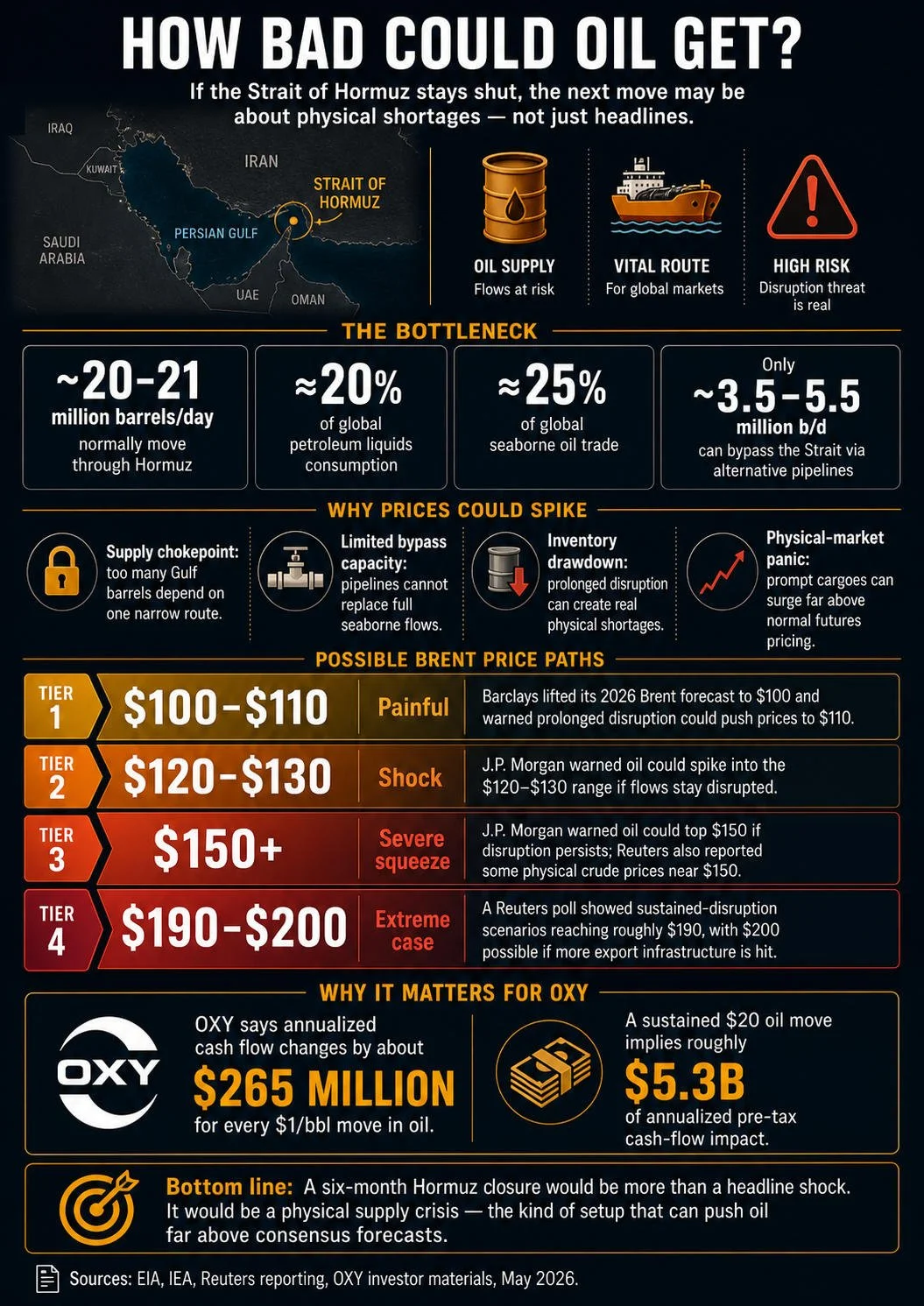

The U.S. Energy Information Administration says oil flows through the Strait averaged about 20 million barrels per day in 2024, equal to roughly 20% of global petroleum liquids consumption. In the first half of 2025, EIA estimated flows averaged 20.9 million barrels per day, equal to about one-quarter of global seaborne oil trade.

The International Energy Agency gives a similar picture: about 20 million barrels per day, or roughly 25% of world seaborne oil trade, normally transits the Strait. The IEA also notes that only about 3.5 to 5.5 million barrels per day of pipeline capacity could potentially redirect crude flows around the Strait. In other words, there is no easy workaround if the waterway remains blocked or severely restricted.

That matters because the market can handle a short disruption. It can dip into inventories. Governments can release strategic reserves. Buyers can reroute ships. Traders can price in a temporary war premium and then fade it when ceasefire headlines appear.

But a six-month closure is different.

A six-month closure is not a headline risk. It is a physical shortage risk.

That is the heart of the OXY bull case.

The Market May Still Be Underpricing Duration

One of the weirdest things about this crisis is that oil has surged, but energy equities have not fully behaved as if the world is facing a long-term energy shock.

Reuters reported that oil majors had seen limited share-price gains despite the oil surge because investors were still expecting the Strait closure to be relatively short-lived. That is important. If the market is still pricing this as temporary, then a change in that assumption could force a second leg higher in oil stocks.

This is where OXY becomes interesting. If traders start believing the Strait will remain shut for months, the trade changes from “oil spike” to “oil regime shift.”

A spike can fade. A regime shift gets modeled into earnings, cash flow, debt reduction, buybacks, and valuation multiples.

Reuters reported that Barclays raised its 2026 Brent forecast to $100 per barrel, citing ongoing Hormuz disruption, and warned that further prolonged disruption could push prices as high as $110. Barclays also reportedly warned of a sustained oil-market deficit due to inventory draws and supply shocks.

That is already bullish for oil stocks. But the really explosive case is not Brent at $100. The explosive case is Brent staying above $110, then pushing back toward $125, $140, or higher if shipping remains restricted and inventories keep drawing down.

Reuters also reported that OPEC+ was considering another output quota increase, but the increase was described as largely symbolic because the continued Hormuz closure had severely affected exports from key Gulf producers. That is exactly the kind of situation where normal supply responses do not work. Producers can announce more supply, but if barrels cannot move through the Strait, the market does not receive them in the usual way.

Why OXY Has More Torque Than the Safer Oil Giants

Occidental is not just “an oil stock.” It is a company whose cash flow is highly sensitive to crude prices.

In its own fourth-quarter 2025 earnings presentation, OXY said annualized cash flow changes by approximately $265 million for every $1 per barrel change in oil prices. That figure includes about $240 million per $1 move in WTI and about $25 million per $1 move in Brent.

That is the key number.

If oil prices move $10 higher and stay there, that is roughly $2.65 billion of additional annualized pre-tax cash flow.

If oil prices move $20 higher and stay there, that is roughly $5.3 billion.

If oil prices move $40 higher from OXY’s planning assumptions, that is roughly $10.6 billion in additional annualized pre-tax cash flow.

Those are enormous numbers for a company with a market cap under $60 billion.

This is why OXY could move so aggressively. The market is not just buying barrels in the ground. It is buying the possibility that a company with a debt-heavy history suddenly gets a massive free-cash-flow windfall at exactly the moment when debt reduction and shareholder returns matter most.

OXY’s own presentation says accelerated debt reduction brought principal debt to roughly $15 billion, and that the company had repaid $13.9 billion of debt in 20 months, reducing annual interest expense by roughly $740 million.

That matters because higher oil prices do not just increase earnings. They can also accelerate balance-sheet repair. A cleaner balance sheet can then support a higher equity multiple. That is where the stock-price upside can become nonlinear.

A simple oil move creates cash flow.

A sustained oil shock creates cash flow, debt reduction, improved investor confidence, and multiple expansion.

That is how a $60 stock can become an $80 stock quickly. It is also how it could become a $100 or $120 stock if the crisis lasts long enough.

What would happen if the Strait were to re-open tomorrow?

It’s not great.

Best case scenario if the Straight re-opens TODAY

The $120 Case Is Aggressive, But the Math Is Not Absurd

At around $58.71, OXY would need to roughly double to reach $120. That sounds extreme until you think about what the market would be pricing.

A $120 OXY would imply a market cap around $118 billion to $120 billion, depending on share count. OXY’s fourth-quarter presentation showed roughly 1.003 billion diluted average shares outstanding in its dilution example.

So the question is not, “Can OXY randomly double?”

The better question is: “Could the market value OXY around $120 billion if oil stays elevated because a chokepoint that handles about one-fifth of global petroleum liquids consumption remains disrupted?”

In a normal oil market, maybe not. In a short panic spike, maybe not. But in a six-month Hormuz crisis, the answer becomes yes.

Imagine WTI and Brent stay meaningfully above OXY’s baseline assumptions for two or three quarters. OXY’s cash-flow sensitivity means every $10 per barrel matters. If the crisis adds $20 to $40 per barrel to realized oil pricing for a sustained period, the company could be generating billions of dollars in incremental annualized cash flow.

That cash can be used to reduce debt, improve the balance sheet, support dividends, repurchase shares, or simply convince the market that OXY deserves a higher valuation.

The market does not need OXY to permanently earn crisis-level cash flow to send the stock higher. It only needs to believe the windfall is large enough, durable enough, and useful enough to transform the balance sheet.

That is the $120 thesis.

Not “OXY is worth $120 forever.”

More like: “OXY could trade to $120 if the market begins pricing a multi-quarter oil shock and a massive cash-flow windfall.”

Why Fall Is the Critical Window

The timing matters.

If the Strait remains severely restricted into May and June, traders may still argue that a reopening is imminent. That is why OXY could chop around, even with oil elevated.

But by July or August, the psychology changes. A temporary disruption that lasts several months stops feeling temporary. Refiners, airlines, shipping companies, governments, and investors all have to start adjusting to a new reality.

That is when the equity market may begin chasing the oil move.

The first target would be $70 to $80. That could happen on headlines, especially if oil pushes back toward recent highs or if analysts begin raising OXY-specific estimates.

The second target would be $90 to $100. That likely requires the market to accept that high oil prices are sticking through the summer.

The third target is $110 to $120. That requires something more extreme: continued closure, rising crude prices, strong OXY cash-flow revisions, and a market that starts treating OXY as a high-beta crisis winner rather than just another energy stock.

This is why “by fall” matters. Fall gives the thesis enough time to move from panic to earnings revisions.

Why OXY Could Move Faster Than Analysts Expect

Analysts often update price targets slowly. Commodity shocks can move faster than models.

That is especially true when the market has been leaning on the wrong assumption. If the consensus assumption is “the Strait reopens soon,” then every week it does not reopen damages that assumption. Eventually investors stop asking when the crisis ends and start asking which companies benefit if it does not.

OXY could attract several types of buyers at once:

Momentum traders chasing oil-linked equities.

Energy investors looking for companies with high crude sensitivity.

Macro funds looking for U.S.-based oil exposure insulated from some Gulf shipping issues.

Options traders looking for convex upside.

Value investors who see faster debt reduction and higher free cash flow.

That combination can create a violent move. A stock does not need every investor to agree it is worth $120. It only needs enough investors to decide they are underexposed to the possibility.

The Main Risks to the $120 Thesis

The biggest risk is obvious: the Strait reopens sooner than expected.

If there is a credible diplomatic deal, safe shipping resumes, and oil starts falling back toward pre-crisis expectations, OXY could drop hard. This is especially true because part of the current energy trade already reflects geopolitical premium.

The second risk is demand destruction. If oil goes too high for too long, the global economy weakens. Reuters has already reported that prolonged energy disruption is feeding stagflation concerns. At some point, extremely high oil prices stop being purely bullish for oil equities because investors begin worrying about recession, falling demand, political intervention, and credit stress.

The third risk is political. If fuel prices explode, governments may intervene. Windfall taxes, export restrictions, fuel subsidies, price caps, reserve releases, and pressure on producers can all reduce the upside investors are willing to pay for.

The fourth risk is company-specific. Reuters reported that OXY CEO Vicki Hollub is retiring on June 1, 2026, with Richard Jackson set to succeed her. Leadership transitions are not automatically bad, but they add another variable during a volatile moment.

The fifth risk is that options traders overpay. OXY can be a great stock thesis and still be a dangerous call-option trade if implied volatility is too high. A trader buying short-dated calls needs not only the right direction, but the right speed. If OXY rises slowly, short-dated calls can lose money even while the stock goes up.

The Bottom Line

OXY to $120 by fall is not the base case. The base case is probably something more like $80 to $100 if the Strait remains severely restricted and oil stays elevated.

But $120 is a legitimate bull-case target if three things happen.

First, the Strait of Hormuz remains closed or nearly closed long enough for the market to abandon the “temporary disruption” narrative.

Second, Brent and WTI remain high enough to create a multi-quarter cash-flow windfall for U.S. oil producers.

Third, investors begin rewarding OXY not just for higher oil prices, but for what those higher prices do to debt reduction, free cash flow, and balance-sheet strength.

That is the real story.

The Strait of Hormuz disaster is not just an oil-price event. It is a duration event. If it lasts weeks, OXY may spike. If it lasts months, OXY may rerate. If it lasts into fall, the market may have to seriously consider numbers that looked ridiculous only a few months earlier.

And in that scenario, OXY at $120 stops looking like a fantasy and starts looking like the kind of aggressive target that markets hit when a supposedly temporary crisis becomes the new reality.

Thanks for reading.