Natural Gas Is Spiking Too: LNG Disruptions Explained

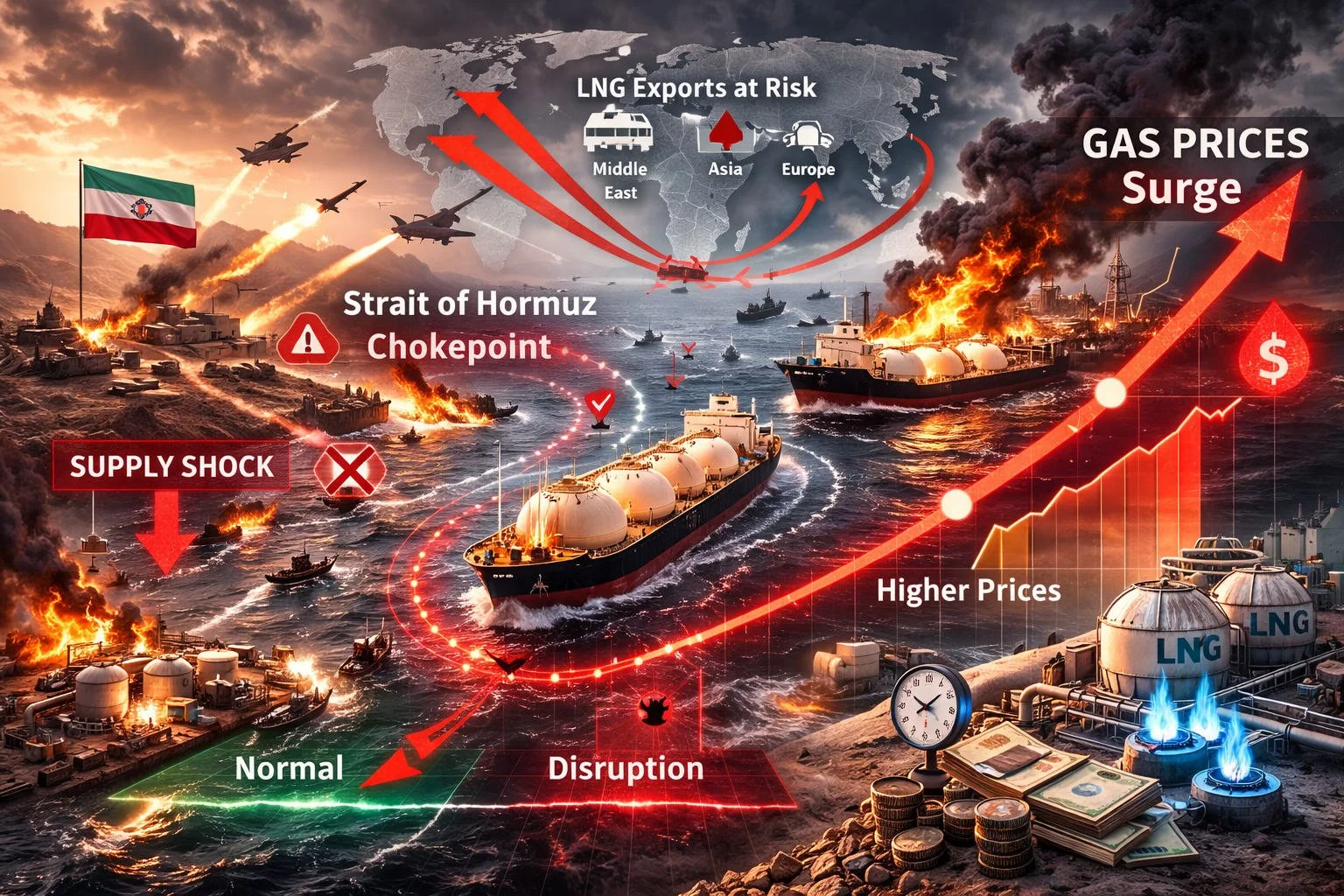

When the Strait of Hormuz shows up in the news, most people think “oil.” But in this war, natural gas is flashing red too—and in some ways, gas markets can react even faster than oil because they’re tighter, more regional, and harder to reroute at short notice.

In the past 24–48 hours, the market has treated LNG risk as immediate: Europe’s benchmark gas price jumped more than 40%, and Asia’s LNG benchmark jumped nearly 39% in a single session.

So what’s actually going on—and why does LNG disruption turn into “gas is spiking” so quickly?

LNG 101 (in 60 seconds)

Natural gas is usually moved two ways:

Pipeline gas (think: steady flow through pipes between neighboring countries)

LNG (liquefied natural gas) (gas is chilled into a liquid, loaded onto tankers, shipped globally, then turned back into gas at import terminals)

LNG is the “global” version of gas. It’s also the version most exposed to shipping chokepoints and war-risk insurance.

Why the Strait of Hormuz matters for natural gas

A massive amount of LNG depends on the Strait—especially LNG from Qatar.

In 2024, about 20% of global LNG trade transited the Strait of Hormuz, primarily from Qatar.

The EIA estimates Qatar exported about 9.3 Bcf/d of LNG through the Strait in 2024 (and the UAE about 0.7 Bcf/d).

Reuters reports Qatar accounts for about 20% of global LNG exports, and that Qatari cargoes must exit via the Strait.

So when Hormuz gets risky, LNG buyers don’t just worry about “price.” They worry about physical delivery.

What’s driving the spike right now

This isn’t one problem—it’s several stacked together.

1) Shipping disruption and “de facto closure” dynamics

The market is reacting to conditions where ships can technically sail but may not be able to insure the voyage or justify the risk.

Reuters reports that tankers have been damaged, vessels are stranded, and marine insurers are canceling war-risk cover, which pushes shipping costs up and can freeze traffic.

For LNG, that matters because LNG cargoes are time-sensitive and the supply chain is less forgiving.

2) Qatar production shock risk

LNG doesn’t just depend on the sea lane. It depends on giant coastal liquefaction facilities that are hard to replace if disrupted.

Reuters reports Qatar halted LNG production after strikes on facilities at Ras Laffan, and QatarEnergy was set to declare force majeure on shipments.

This is exactly the kind of headline that turns “risk premium” into “buyers panic.”

3) Pricing agencies are literally suspending parts of the market process

When even price-assessment mechanisms start pausing normal operations, that’s a sign the market has entered “abnormal conditions.”

Reuters reports S&P Global Platts suspended bids/offers for some LNG price assessments connected to Strait-of-Hormuz shipping, citing major shipping disruptions and safety concerns.

That’s not a small technical footnote—it's a signal that routine trade is being disrupted at the plumbing level.

The benchmarks that prove this is real (not just vibes)

Gas markets have clear “thermometers.” Two of the biggest:

Europe (TTF): Reuters reports the Dutch front-month TTF contract was up more than 40% to 45.38 euros/MWh.

Asia (JKM): Reuters reports the Japan-Korea Marker (JKM) was up almost 39% to $15.068/mmBtu.

Those are massive moves by natural gas standards—especially when they happen this fast.

Why Europe and Asia are the “blast radius” for LNG disruption

Even if North America has plenty of gas, global LNG is a balancing system—and Europe/Asia are where the shock lands first.

Reuters (citing Vortexa) says LNG exports to Asia and Europe are the most exposed if Hormuz is closed, and warns there’s “no spare capacity in the LNG market,” making disruption “immediate and immense.”

Vortexa’s numbers highlight why Asia is especially vulnerable:

Over 90% of Qatar’s LNG exports pass through the Strait.

That puts Asian buyers most at risk—Vortexa estimates 25% of Asia’s total LNG supply and 30% of China’s LNG flow go through this chokepoint.

Europe is also exposed because Europe has leaned harder on LNG in the post-2022 era, and “replacement cargoes” often come from the same finite global spot pool. When fear hits, Europe and Asia bid against each other.

Why LNG shocks can feel “worse” than oil shocks

Oil is global, liquid, and widely substitutable. LNG is global-ish, but logistics-constrained.

A few reasons LNG disruption can hit harder, faster:

Long-term contracts dominate. Reuters notes Qatar sells most of its LNG under long-term contracts, with only a smaller slice in spot. That means the “free” supply available to redirect in a crisis is limited.

You can’t reroute LNG instantly. It’s not like crude where refiners can swap grades. LNG needs compatible terminals, regas capacity, and shipping availability.

There’s less slack. If the market truly has little spare LNG capacity (as Vortexa warns), even small disruptions force big price moves.

The real-world ripple effects (what people notice)

If LNG disruption continues, the pain doesn’t stay inside energy trader screens:

Electricity prices rise (gas-fired power becomes more expensive)

Industrial costs jump (chemicals, cement, steel, glass)

Fertilizer prices rise (gas is a key feedstock for ammonia)

Inflation pressure returns (energy is the “tax” inside everything)

And here’s the nasty feedback loop: higher gas prices can push some users to substitute toward oil products, adding upward pressure on oil too—especially during a broader Middle East shock.

What to watch next (simple, practical signals)

If you want to gauge whether the gas spike is a one-week panic or a longer crisis, watch these:

Do insurers restore war-risk coverage in a way shipowners accept—or does coverage stay canceled/expensive?

Does Qatar resume normal LNG operations, or do force majeure conditions spread?

Do benchmark prices keep “holding gains” day after day (TTF/JKM staying elevated), rather than snapping back?

Do more LNG-related market mechanisms pause (like assessment changes and shipping suspensions)?

Bottom line

Natural gas is spiking because LNG is uniquely vulnerable to the kind of disruption now unfolding: a chokepoint shipping lane, war-risk insurance stress, and concentrated production in a small number of mega-facilities—especially Qatar.

Oil shocks make headlines. LNG shocks hit power bills and factories fast. And right now, the market is telling you it believes this is not a minor side story. 🚨